The secret to early retirement in one sentence?

Maximise your savings rate.

This seems kind of obvious. Spend less than you earn. When it comes down to it, the percentage of what you save compared to what you earn is ultimately what defines how long you need to work for. Sure, the return on your investment has an effect on this as well, especially if you are only saving money in your superannuation fund. But you have limited control on your investment returns, where as you are solely responsible for your savings rate. The higher your savings rate the less the investment return matters.

We have already looked at how much you need to retire with the 4% rule. But it can be

hard looking at saving such a large sum of money and it can seem so far away. So

today we will look at things in a simple way to make the retirement goal more achieveable.

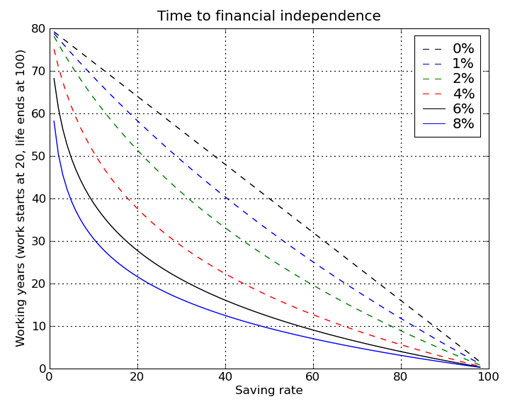

Let's look at the following graph.

Maximise your savings rate.

This seems kind of obvious. Spend less than you earn. When it comes down to it, the percentage of what you save compared to what you earn is ultimately what defines how long you need to work for. Sure, the return on your investment has an effect on this as well, especially if you are only saving money in your superannuation fund. But you have limited control on your investment returns, where as you are solely responsible for your savings rate. The higher your savings rate the less the investment return matters.

We have already looked at how much you need to retire with the 4% rule. But it can be

hard looking at saving such a large sum of money and it can seem so far away. So

today we will look at things in a simple way to make the retirement goal more achieveable.

Let's look at the following graph.

You can see from the graph that if you save 10% of your income, and if the return on investment is 4% (after inflation), you will need to work for about 50 years. This is roughly what compulsory superannuation will do. To retire early you need to do better than this. Even if you can only manage to save another 10% on top of this you will drop your working life by about 13 years. If you are earning $50 000 a year after tax, you only need to save an extra $5000 a year to save yourself an extra 13 years of work! This is good news. By reading through the previous posts on house insurance, and car costs, you should be able to save a few thousand dollars already. Hopefully more. In coming posts we will talk about little things that add up to large savings, not by being cheap, but just by being efficient.

Here at ERA, I am aiming for a 75% savings rate. So with 4% returns, starting from scratch, I would be able to retire in about 9 years. So why aren't I there yet? After all I have been working for close to 13 years.

I was not always aiming for early retirment and in my younger days I wasn't concerned with saving money all that much. I went on a working holiday to the UK and did a fair amount of travelling. These were experiences I enjoyed but they have set back the early retirement date. But even with the travelling I was probably still saving about 40% of my income on average. It's only in the last few years that I have ramped it up by becoming aware of my goal.

I know a 75% savings rate may not be possible for everyone, but I am sure that most people can do a little better than their current savings rate by making just a few of the changes we talk about here.

The other way to increase your savings rate is by increasing your income (without increasing your spending). If you are at the low end of the savings rate, getting a pay rise can be a very effective way to increase your savings rate, but once you get to the high end of the savings rate scale your income makes less of a difference. If I earnt twice as much as I currently earn, and we will even ignore the extra tax payable, my savings rate would go up to around 88% (a substanial jump), but this would only reduce my working life by about 3-4 years. If someone was saving only 10% of their income, and their income doubled then they would reduce their working life by about 35 years.

What is your savings rate? Can you make any changes to maximise it? I hope you find something you can work on.

See you in the new ERA.

Here at ERA, I am aiming for a 75% savings rate. So with 4% returns, starting from scratch, I would be able to retire in about 9 years. So why aren't I there yet? After all I have been working for close to 13 years.

I was not always aiming for early retirment and in my younger days I wasn't concerned with saving money all that much. I went on a working holiday to the UK and did a fair amount of travelling. These were experiences I enjoyed but they have set back the early retirement date. But even with the travelling I was probably still saving about 40% of my income on average. It's only in the last few years that I have ramped it up by becoming aware of my goal.

I know a 75% savings rate may not be possible for everyone, but I am sure that most people can do a little better than their current savings rate by making just a few of the changes we talk about here.

The other way to increase your savings rate is by increasing your income (without increasing your spending). If you are at the low end of the savings rate, getting a pay rise can be a very effective way to increase your savings rate, but once you get to the high end of the savings rate scale your income makes less of a difference. If I earnt twice as much as I currently earn, and we will even ignore the extra tax payable, my savings rate would go up to around 88% (a substanial jump), but this would only reduce my working life by about 3-4 years. If someone was saving only 10% of their income, and their income doubled then they would reduce their working life by about 35 years.

What is your savings rate? Can you make any changes to maximise it? I hope you find something you can work on.

See you in the new ERA.

RSS Feed

RSS Feed